3 Easy, Money-Saving Budget Templates You Can Create In Google Sheets

SHARE

Unsplash/Juliette Leufke

Spending money is often easier than saving it. If you’re not careful with the number of lattes you sip and bagels you buy, you can rack up debt and spend beyond your means. So it’s time to take control of your finances and finally start budgeting like a boss. Here’s how to create a budget spreadsheet using Google Sheets.

Take inventory of your financial situation.

First things first. Look at your paystubs to understand your take-home pay and the amounts you’re contributing to insurance, retirement and taxes.

For example, let’s say you make an annual salary of $60,000, receiving 26 paychecks per year and live in New York. You contribute 5 percent of your pre-tax income per paycheck to your 401(k), pay $150 per paycheck for medical, dental and vision insurance, and also pay the standard state and federal taxes. This leaves you with a take-home pay amount of about $1,460 every other week. If you have a side hustle, be sure to calculate in any earnings from that as well. For instance, you might write freelance articles for a website, earning $200 per month.

We’ll use the above examples as the monthly income to show how to create a budget spreadsheet in Google Sheets, but if you don’t have a pay stub handy and want to calculate your own take-home pay, there are salary paycheck calculators out there that can crunch the numbers for you.

Understand the percentage-based budget.

In a percentage-based budget, there are three numbers you need to know: 60, 20 and 20. This breakdown helps guide you in your monthly budget. Sixty percent of your take-home pay should be used for life’s necessities — rent, groceries, car insurance, utility bills, student loans, etc. After that, 20 percent goes toward your savings, and 20 percent is left for you to use for whatever your heart desires. This type of budget allows for flexibility, like paying more for your living expenses.

Tip: Consider “paying yourself first,” AKA the money you put into your savings, a monthly bill. You’ll be more likely to pay it every month, which allows you to save more every year, helping you reach more of your financial goals.

Start budgeting.

Now that you know how much your take-home pay is and how you’ll be breaking down your monthly finances, you can begin making a spreadsheet in Google Sheets to track your progress. Let’s look at three sample budgeting templates that are easy to make in Google Sheets.

Simple:

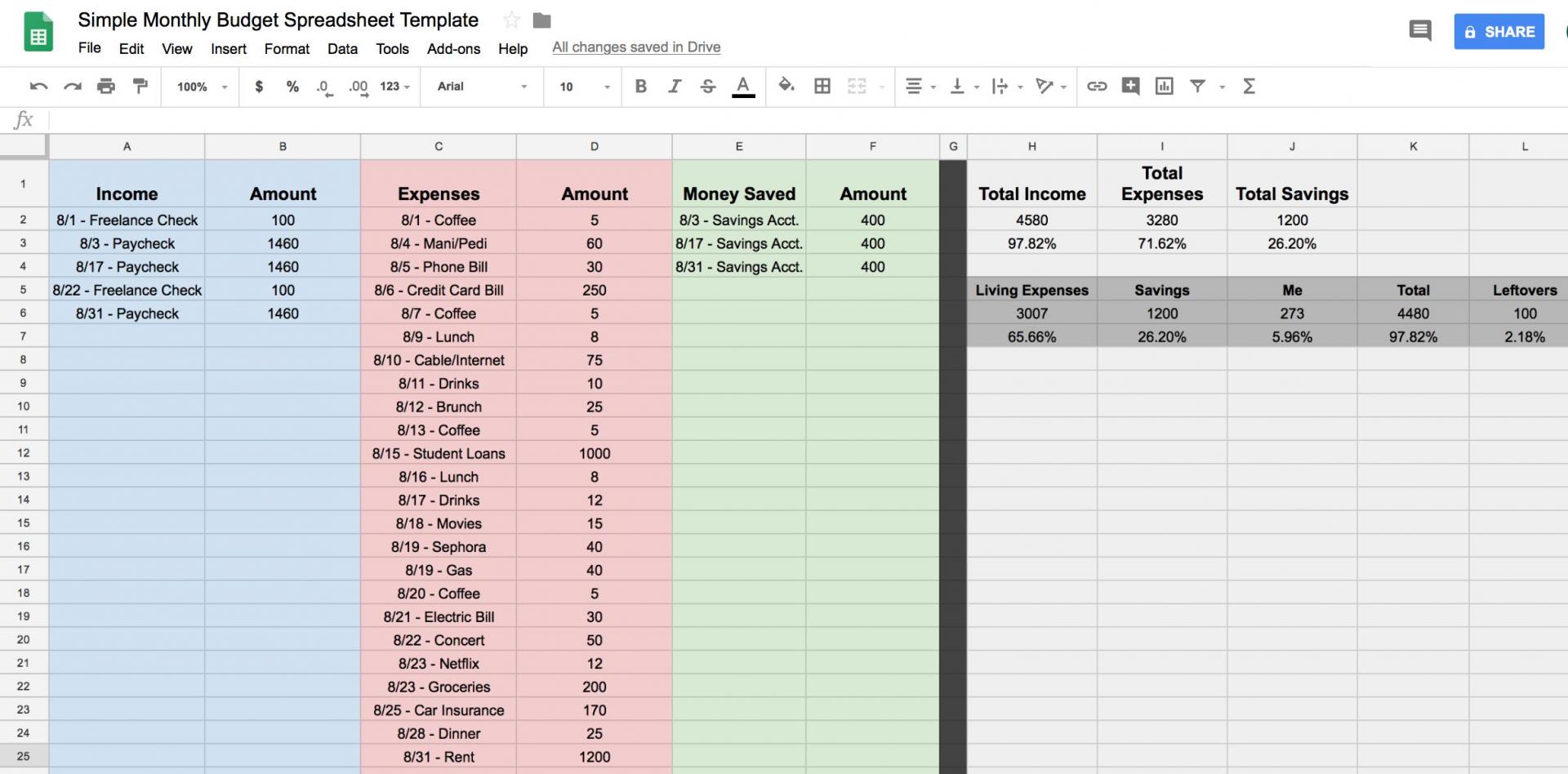

Swirled/Hilarey Wojtowicz

If you’re someone who doesn’t want budgeting to feel like a chore, this spreadsheet is for you. It’s simple and keeps everything together in three simple categories: income, expenses and savings. All you need to do is divide the sheet into four sections — income, expenses, savings and total — and fill in the blanks. We’ve color-coded the spreadsheets in this piece to help each of these sections stand out.

Every month, keep track of your income by documenting each paycheck in that column, every individual purchase you make in the expenses area and any contributions you make to your savings account in that column. Of course, if you have any other accounts like investments, add a section to the sheet and keep track of it all.

Use the simple Google functions to sum up the amounts in each of the sections into the total areas (the gray boxes). For instance, in the “Total Income” cell it says “4580,” which is the total take-home pay for the month when you add up all the amounts in the income section. Do this for the expenses and the savings cells, too.

Now break down the amounts you spend on expenses, savings and extras (the “Me” section on this spreadsheet) and calculate the percentages by dividing each one over the total amount of income for the month. This will allow you to see how the amounts you spend on expenses and savings fit into the 60-20-20 percentage-based budget rule.

In this hypothetical budget example, 65.66 percent of the monthly income is going toward living expenses, 26.20 percent is going toward savings and only 5.96 percent is going toward whatever you want. This also shows that there is $100, or 2.18 percent of your monthly budget left, which could go toward whatever you want, savings or expenses. Even though this example shows that the amounts for expenses and savings are over 60 and 20 percent, the percentage-based budget allows for flexibility like this so that you can stress less about your monthly finances.

More Detailed:

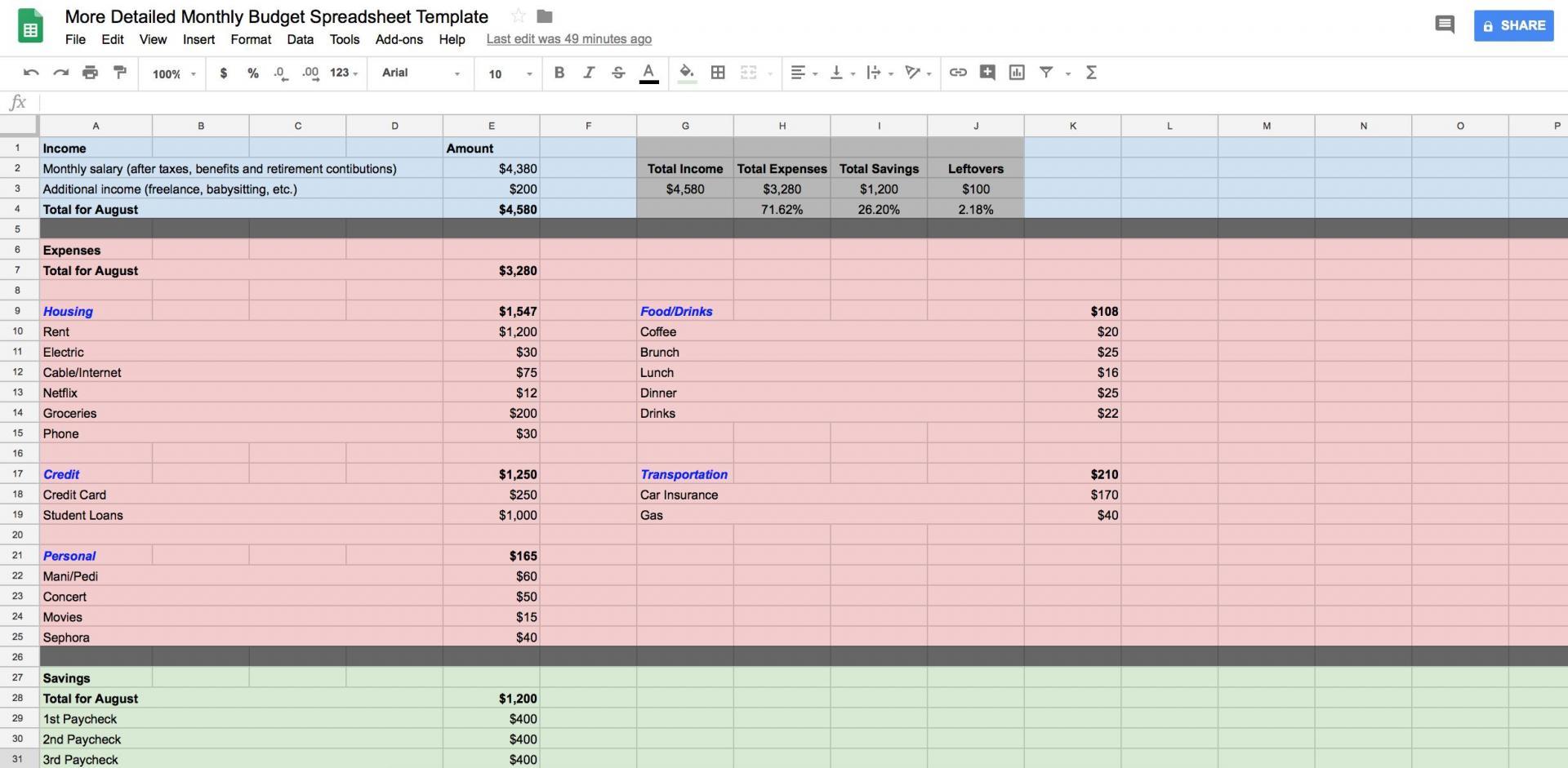

Swirled/Hilarey Wojtowicz

This spreadsheet does the same job as the simple version, but it breaks down the expenses into more detailed subcategories. As you can see, the expenses section now has areas for housing, credit, personal, food/drinks and transportation. It also keeps the 60 percent for life’s necessities and the 20 percent for whatever you want together in the same expenses category.

The best part about this more detailed budget template is that you can assess if you feel you’re overspending in one area of your expenses, such as food/drinks. This allows you to cut back in specific areas from month to month and, ultimately, save more money.

Master Budget:

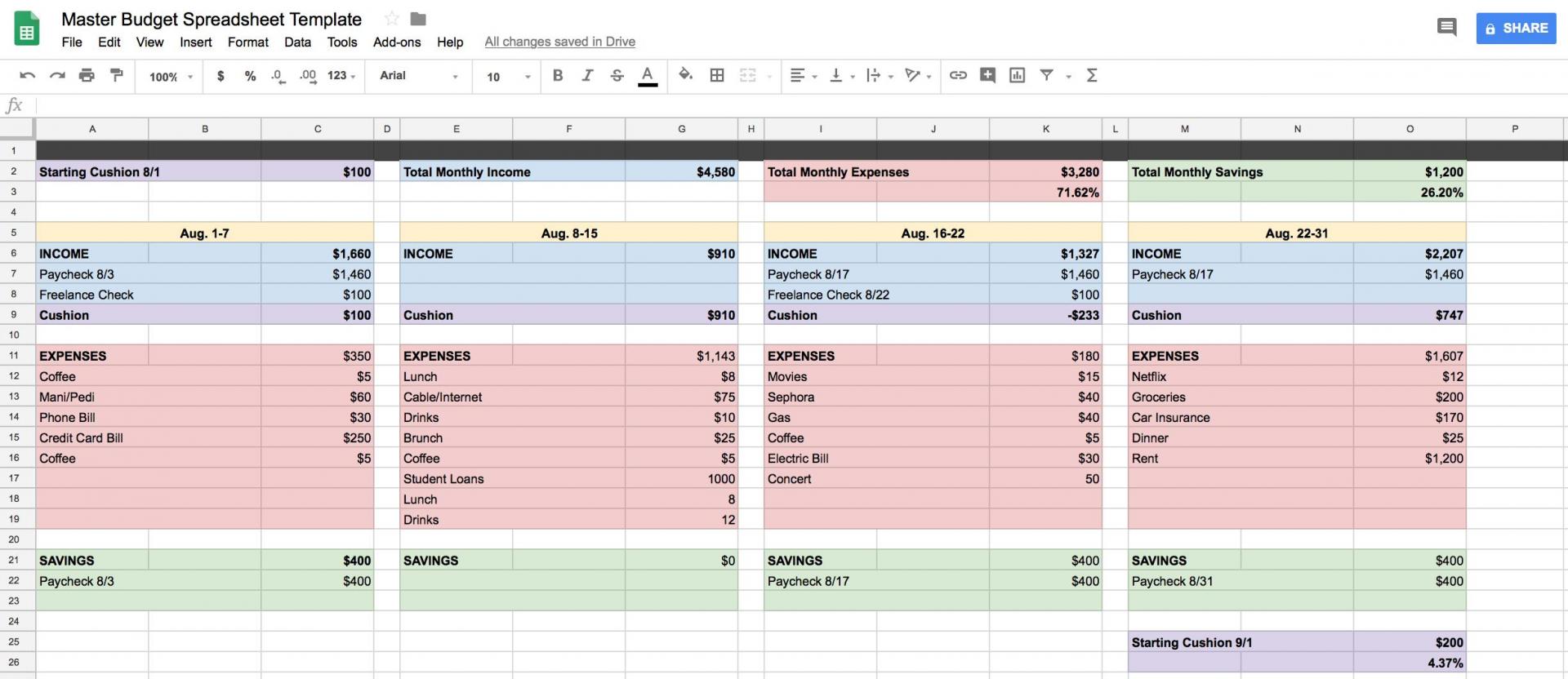

Swirled/Hilarey Wojtowicz

If you’re looking to save money from week to week throughout each month, then this master budget template is for you. You’re still tracking income, expenses and savings through the lens of the 60-20-20 percentage-based budget, but this time, you start with a cushion.

The cushion is the amount you have left over from the month before. Every week the cushion rolls over, too. For instance, in this example above, you’ll see that during the first week of Aug. 1-7, there is a $100 cushion listed in purple below the income section. This $100 gets added to the income total for that week, so you’re total income is $1,660. Subtract that week’s expenses from that week’s income. This shows you what you have leftover for the next week, which becomes the cushion for the week of Aug. 8-15, and so on and so forth.

As you can see, the cushion and income for the week of August 8-15 is $910, but the expenses are pretty high during that week — $1,143. This means the cushion for the week of August 16-22 is negative (-$233). However, you received a paycheck on Aug. 17, which replenished that negative cushion, giving you $747 going into the week of August 23-31. During that week, you received one last paycheck, paid the last few bills, and ultimately ended the month on a high note, with a cushion of $200 going into September. Now you can do it all over again for that month, with a goal to have an even larger cushion by October 1.

It’s all about the budget.

These budget templates are super simple to make in Google Sheets, but it’s important to use a budget template that works best for you. All that matters is that you’re aware of your spending and saving habits because budgeting is the first step toward living a fierce financial life and thriving every day.

Sign up for Savvy Saver by Swirled, our newsletter featuring budget hacks and important (yet fun) financial info. Saving money just makes cents!

RELATED

5 Smart Budgeting Apps That Will Help You Keep Your Life Together

Here’s How To Budget If You’re In The Middle Of A Job Change

How To Successfully Budget With An Inconsistent Income

Next on