How To Decode Your Credit Score Like A Pro

SHARE

Flickr/Sean MacEntee

We’re not gonna lie — we’re regularly mystified by our credit scores. Some people prefer to ignore their credit scores and just do what they can on a day-to-day basis while others are full-on obsessed. Whether your score is good or not, you should know exactly why it is the way it is. So here’s the low down on what your credit score means, how it’s affected and what it’s made of.

The Bureaus

Your credit score report is calculated by credit bureaus, the major ones being Equifax, Experian and TransUnion. These organizations collect financial data on you to sell to those interested in your credit history (like lenders, landlords and potential employers). You can read more about each bureau here. You may also be familiar with FICO®, which is a single score in which these bureaus have synthesized all of your data. When checking your score, you’re most likely looking at FICO®.

The FICO® Score Range

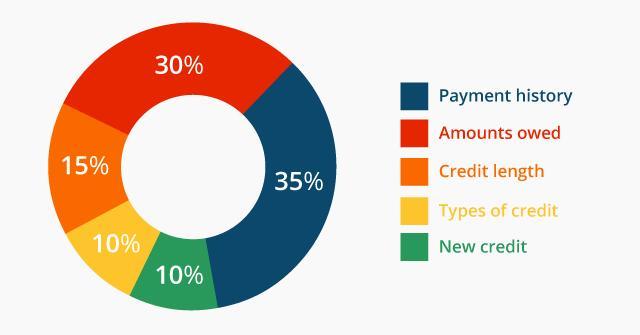

While all bureaus’ scores can vary, your FICO® score could be anywhere from 300 to 850. What factors decide your overall score? Payment history, amounts owed, credit length, types of credit and new credit (in their respective percentages) affect your score. Payment history specifically refers to any late payments or delinquency while amounts owed is the physical amount of debt you still have to pay. Credit length is how long all your lines of credit have been open and active, types of credit are the different ways you pay for (or spend money on) things — think credit cards, student loans, mortgage payments, etc. New credit, of course, refers to any new lines of credit you’ve opened, like a new store credit card.

Flickr/CafeCredit.com

It’s important to remember that your credit score shifts, so don’t panic if your number goes up and down a little from time to time.

Checking (And Comparing) Your Score

You’re entitled to a free annual credit report through AnnualCreditReport.com. This website is a portal for you to see reports from all three major credit bureaus. If you have access to reports through your bank, take full advantage, but know that you’re probably not getting all three major reports. Interested in purchasing all three reports? (You’ll want to do this if a potential landlord, for example, wants to see your “full” credit score) You can buy them from FICO or Experian.

Don’t fret if you don’t have an amazing score — according to a 2018 FICO analysis, the average score for 18- to 29-year-olds is 652, which is a middle-of-the-road score.

What Your Score Means For Your Lifestyle

You’re probably already aware that your credit score could dictate what credit cards you can and cannot be approved for, what loans you can get, which apartments you can rent and more. What’s wild is that all of these things can also dictate what your score looks like. It’s a symbiotic relationship between your score and your lifestyle. They have to have balance, and you have to treat your money well.

Next on